The Indian Art Market Comes of Age

Understanding the Indian Art Market in 2026: Growth, Records, Risks and New Opportunities

For much of the late twentieth century, the Indian art market was viewed as a promising but relatively niche segment of the global art economy. While India possessed one of the world’s richest artistic traditions, its market remained modest compared to established centres such as New York, London, Paris, or Hong Kong.

That narrative is changing rapidly.

As of 2026, the Indian art market has entered what may be described as a phase of mature expansion. While major international markets—including the United States, China, and parts of Europe—have experienced periods of contraction, India has emerged as one of the fastest-growing art markets globally. Rising domestic wealth, increasing institutional interest, stronger scholarship, and growing cultural confidence have collectively transformed the landscape.

The story is no longer merely about record prices.

It is about the emergence of a more sophisticated collecting culture.

A Market Growing in Scale and Confidence

The total size of the Indian art market—including auctions, galleries, private sales, art fairs, and online transactions—is now estimated at approximately ₹5,500–6,000 crore (USD 650–720 million).

Auction turnover for FY 2024–25 stood at approximately ₹1,620.6 crore (USD 193 million). Although this represented a marginal decline of 4.6% from the previous financial year, the decrease was largely due to fewer works being offered at auction. More importantly, average sale prices increased by over 7%, reaching approximately ₹42.3 lakh per lot.

In practical terms, collectors purchased fewer works but paid significantly more for quality.

This distinction is important because mature markets are often defined not by volume alone but by increasing selectivity.

Another major structural shift has been the rise of domestic buyers. Unlike earlier decades, when international collectors and Non-Resident Indians played a dominant role, domestic participation now accounts for an estimated 60–80% of sales across several market segments.

India’s broader economic growth has undoubtedly contributed to this trend. With GDP growth projected at approximately 7.3% for 2025–26 and a growing population of entrepreneurs, professionals, and family offices, art is increasingly being viewed as both a cultural asset and a long-term store of value.

The reduction of GST on artworks from 12% to 5% in September 2025 further strengthened market sentiment by improving liquidity and encouraging broader participation.

The Era of Record-Breaking Prices

The most visible evidence of confidence in the market can be found in the extraordinary auction records established over the last two years.

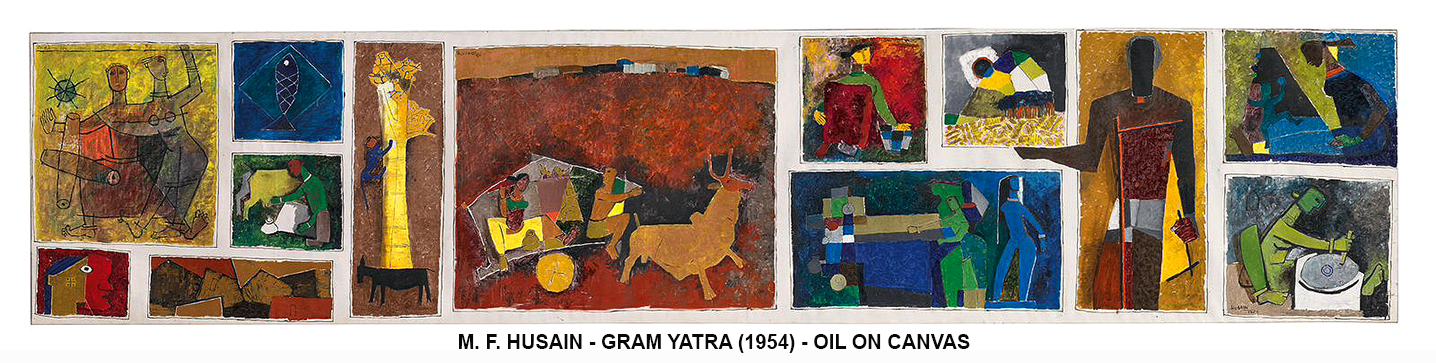

In March 2025, M. F. Husain achieved a historic milestone when his monumental Gram Yatra (1954) sold for approximately USD 13.8 million (around ₹118 crore) at Christie’s New York, setting a new benchmark for modern Indian art.

That record was surpassed in April 2026 when Raja Ravi Varma’s celebrated Yashoda and Krishna achieved approximately USD 17.9 million (around ₹167.2 crore), establishing a new all-time record for any South Asian painting sold at auction.

These landmark sales reflect more than market enthusiasm. They indicate increasing recognition of India’s artistic heritage at the highest levels of international collecting.

The strength of the market has not been limited to a handful of iconic names.

The combined auction turnover of Husain, S. H. Raza, and F. N. Souza exceeded USD 40 million during 2025 alone, reinforcing the continuing dominance of India’s modern masters.

Meanwhile, the market has also witnessed renewed appreciation for historically significant artists whose importance extends beyond headline-grabbing records.

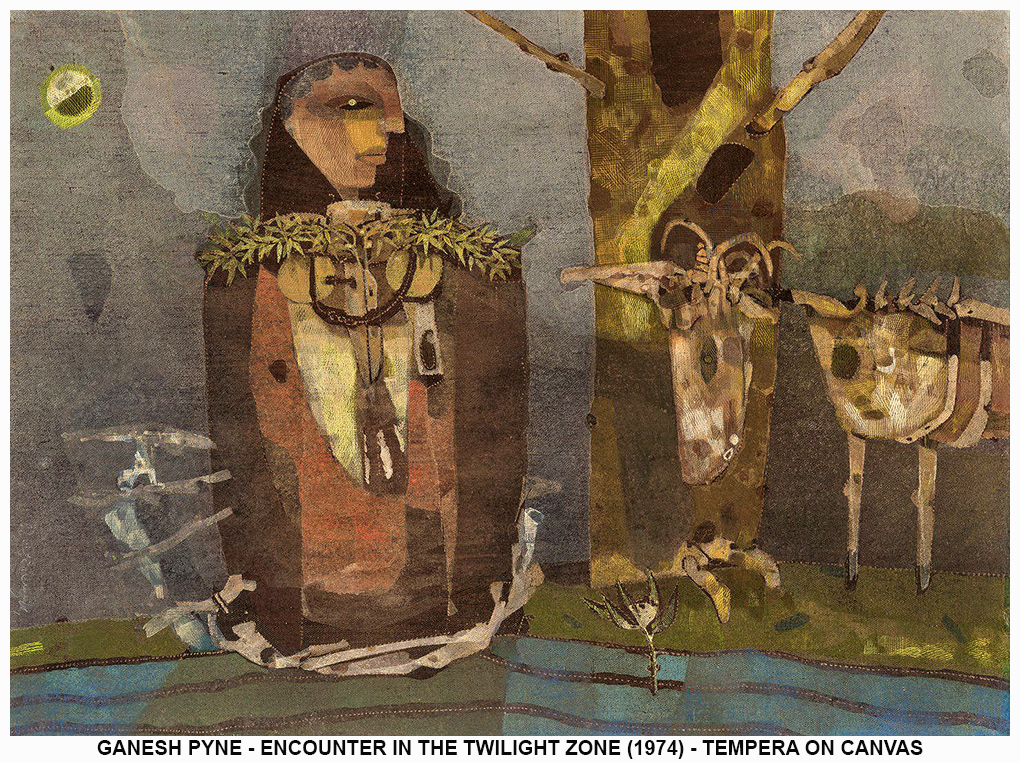

A particularly notable example is Ganesh Pyne, one of the most intellectually respected figures in modern Indian art. Long admired by scholars, artists, and serious collectors, Pyne’s market has experienced a remarkable resurgence in recent years. His 1970 painting Untitled achieved approximately USD 787,400 at Sotheby’s in 2025, setting a new auction benchmark for the artist and significantly surpassing previous records.

More recently, Christie’s has continued to spotlight Pyne’s importance through major sales and dedicated presentations, reflecting growing international recognition of his poetic, psychologically charged visual language. (Christie’s)

The increasing demand for artists such as Ganesh Pyne suggests that collectors are looking beyond market trophies and engaging more deeply with historically significant practices.

Five Years That Reshaped the Market

The period between 2021 and 2026 may ultimately be viewed as one of the most transformative phases in the history of the Indian art market.

Following the uncertainty of the pandemic years, the market rebounded with surprising strength. Initially driven by online auctions and deferred demand, the recovery gradually evolved into a broader expansion encompassing galleries, private sales, fairs, and international participation.

Between 2021 and 2024, entry-level prices for several blue-chip artists rose dramatically. In certain segments, acquisition costs for important works by leading masters increased by nearly 287%.

By 2025 and 2026, however, growth became increasingly selective.

Rather than indiscriminate buying, collectors began focusing on rarity, provenance, exhibition history, scholarly importance, and historical relevance.

This transition is a healthy sign.

Markets driven entirely by speculation tend to be volatile.

Markets supported by research and connoisseurship tend to be more sustainable.

Recent reports indicate that activity within the ₹1–10 crore category increased by over 50% year-on-year, reflecting strong demand for museum-quality works and historically important material.

The Concentration Challenge

Despite impressive growth, the Indian art market continues to face a structural challenge.

Although more than 1,000 artists have appeared at major auctions in recent years, a significant percentage of total value remains concentrated among fewer than twenty names.

Artists such as Husain, Raza, Souza, Ravi Varma, V. S. Gaitonde, Tyeb Mehta, and a select group of others continue to dominate the upper end of the market.

This concentration creates confidence but also limits broader market depth.

Historically, however, such concentration tends to evolve.

As scholarship expands and institutions invest more seriously in research, overlooked artists often begin attracting renewed attention.

The history of global art markets repeatedly demonstrates that today’s secondary figures can become tomorrow’s rediscovered masters.

Scholarship Is Becoming a Market Driver

Perhaps the most encouraging development in the Indian art ecosystem is the growing importance of scholarship.

Collectors today increasingly demand documentation, provenance records, archival research, exhibition histories, artist monographs, and catalogues raisonnés.

This shift is changing the market.

Artists who were previously neglected due to limited documentation are gradually entering mainstream conversations. Regional modernists, early academic painters, printmakers, sculptors, women artists, and historically overlooked movements are beginning to receive serious attention.

The rediscovery of value is often preceded by the rediscovery of knowledge.

Many of the strongest market movements of the future are likely to emerge not from speculation but from research.

Where Future Opportunities May Lie

The highest-profile artists will undoubtedly continue attracting institutional and high-net-worth demand. However, some of the most interesting opportunities may exist outside the obvious blue-chip segment.

Areas receiving increasing attention include historically important modern artists outside the established canon, significant regional modernist movements, Indian printmaking traditions, modern and contemporary sculpture, women artists with renewed scholarly visibility, works supported by strong provenance and archival documentation, and artists whose historical importance exceeds current market valuation. As the market matures, collectors are increasingly rewarding knowledge rather than fashion.

Looking Ahead

The Indian art market of 2026 is no longer merely an emerging market.

The Indian art market of 2026 is no longer merely an emerging market.

It is becoming a mature cultural economy supported by domestic wealth, expanding scholarship, stronger institutions, and growing confidence in India’s artistic legacy.

The record-breaking sales of Ravi Varma and Husain may dominate headlines, but the deeper story is more significant.

It is the story of a country increasingly recognising the value of its own cultural history.

Challenges remain. Market concentration, liquidity concerns for mid-tier artists, and periodic speculation will continue to shape the landscape.

Yet the long-term direction appears clear.

The future of the Indian art market will not be defined solely by wealth creation.

It will be defined by knowledge creation.

For collectors, galleries, scholars, and institutions alike, the greatest opportunities may lie not in chasing the most expensive names but in identifying quality, historical significance, and intellectual value before the wider market fully recognises them.

The Indian art market is growing.

More importantly, it is growing up.

Note : The market figures, auction trends, and artist records discussed above are based on publicly reported auction results and recent market analyses, including major sales involving M. F. Husain, Raja Ravi Varma, and Ganesh Pyne.

- Research & Compiled by Aakriti Art Gallery team

Comments

Join the Discussion

Please login to post comments.

Login